Over the past few months, we have spoken about the need for constraint optimization from public macro policy. The constraint is being set by higher dollar and dollar rates, in turn an outcome of the continued so-called US exceptionalism. This has put obvious limits on economies that don’t print reserve currencies of the world. Optimization is desirable in any circumstance but more so now given the cumulative output gap that we are still facing versus a no-pandemic trend rate of growth. Thus, the ask from India’s monetary and fiscal policy has been to continue laser-sharp focus on preserving financial stability (given a hostile global funding environment) but at the same time to not lose any opportunity to support local growth to the extent possible (given the cumulative output gap).

Policy thus far has largely delivered on this, and RBI also seems now to be proactively addressing the earlier delay in responding to permanent liquidity drain. However, the local growth environment has changed somewhat with real growth downshifting by at least 50 bps from even very recent assessments. To clarify, a short cycle bounce is very much underway from the lows printed in the September quarter GDP on the back of revival in government spending and stronger agricultural production. However, a more persistent drag is also unfolding from leveraged consumption slowing and higher business investment uncertainty from Trump tariffs and the risks from China exporting out its excess capacity. The budget today was set against this backdrop and was a sound exercise in constraint optimization, in our view.

Optimization

1. To start off, fiscal credibility has continued with the government delivering on near term fiscal commitments by targeting a 4.4% deficit for FY26. The more medium term framework is equally assuring with the mission statement being: “the Government would endeavour to keep fiscal deficit in each year (from FY 2026-27 till FY 2030-31) such that the Central Government debt is on declining path to attain a debt to GDP level of about 50±1 per cent by 31st March 2031 (the last year of the 16th Finance Commission cycle)”. This entails an approximately 1% debt to GDP reduction per annum and throws up annual fiscal deficit targets of between 4 – 4.5% as per our calculations. Importantly, this needn’t be done linearly and therefore allows for short term cyclical fiscal responses as well to a limited degree.

2. While states have more obviously been pivoting more towards revenue spending, there was a need for the center to take consumption oriented measures as well, in light of the ongoing slowdown in leveraged consumption. The slowdown in unsecured lending seems to have legs as seen from financial sector commentaries and hence a fiscal consumption boost was very much in order. Even as some part of it may end up getting saved, it will serve the important purpose of augmenting household resources pending a sustained rise in aggregate incomes.

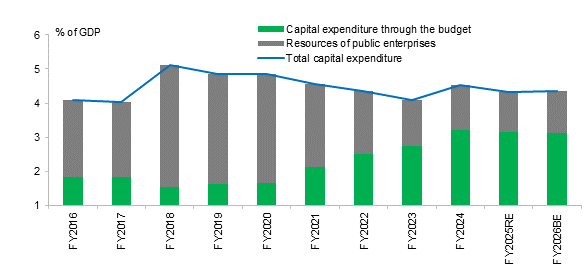

3. While capex spending is rising, it is largely at nominal GDP growth rate and the growth is versus revised numbers for FY 25. Budget FY 25 to 26, on the other hand, is up only modestly. However, if this is a source of disappointment it shouldn’t necessarily be. There are overall resource constraints in play in an environment where some pivot towards boosting consumption was required. Also, there is a question of absorptive capacity as well though we are no experts in this area. A point to note also is that overall capex spending has largely been constant over the past few years. Rather, there has been a shift from using resources of public sector enterprises to onboarding a lot of this spending directly into government fiscal accounts.

Constraints

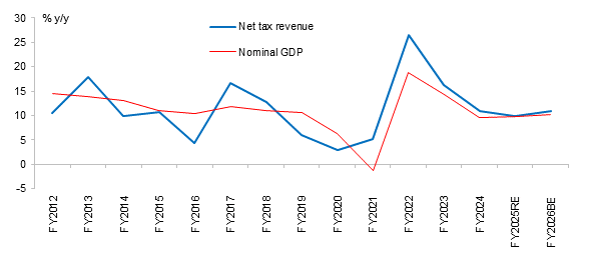

We turn next to a brief discussion on the emerging budget constraints and what they may mean for the way ahead (Note: source for all charts below: CEIC, India Union Budget, Bandhan MF Research).

1. The higher tax buoyancy from greater formalization, asset market support, rise in profit pools etc is now normalizing.

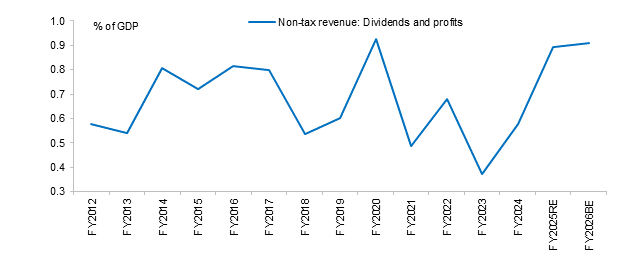

2. Non tax revenue from dividends and profits has ballooned lately reflecting bumper dividend from RBI, as also to some extent stronger performance of PSU enterprises. While the former of this is in play for FY 26 as well, it is difficult to rely on it as a perpetual source of revenues.

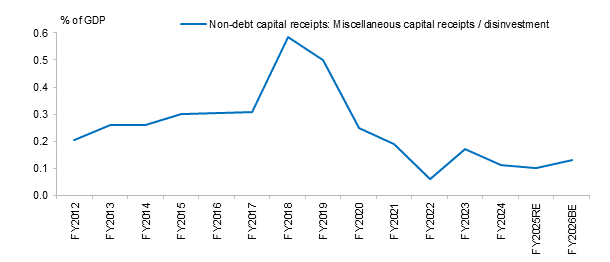

3. As dividends and profits normalise, government will have to shift more attention to divestment receipts which have lagged despite very robust capital markets.

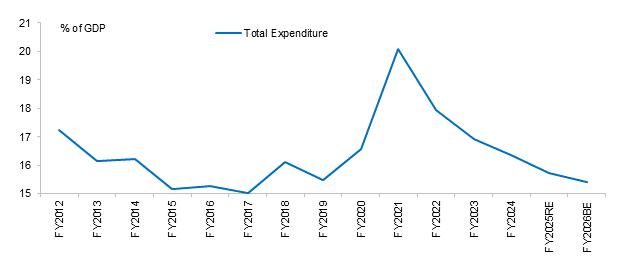

4. As the post Covid fiscal compression has kicked in, total expenditure to GDP has been coming off. Prima facie this implies a ‘handover’ underway from government to the private sector on incremental growth drivers. Given medium term fiscal responsibilities, as well as considering a sustainable template for long term growth, this is exactly how it should be. However, the other notable point in the chart below also is that it is unlikely that government expenditure as proportion of GDP can fall further from here with us now at pre-pandemic levels.

This raises some important points:

a. For this ratio to stabilise, expenditure growth rate has to start matching nominal GDP growth rate from some point in the future as opposed to growing below it currently. If fiscal targets have to be met when this happens, and new buoyancy cannot be found on taxes, then capital receipts have to pick up.

b. It is possible that overtime some capex spending moves back towards resources of public sector enterprises.

5. Continuing from point “b” above, total capex spending as a proportion of GDP has been largely flat over the past few years. Rather, there has been a shift from using resources of public sector enterprises to using the center’s fiscal funding directly.

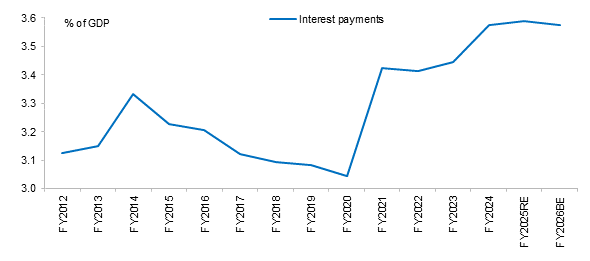

6. Finally, with the stock of debt rising, interest expense has crept up further denting fiscal flexibility.

In summary then, the government has done a fine job of balancing constraints with both short and medium term priorities. The fact remains, however, that the baton of driving growth needs to now move to the private sector. For the time being, with local demand somewhat muted and with higher global uncertainties it may be a shade too optimistic to expect broad based private sector capex revival. However, hopefully as US exceptionalism peaks (we have delved in detail on this topic in a recent presentation titled “Global and India Macro and Markets – Jan-2025 which can be found amidst the presentations available here: https://bandhanmutual.com/downloads/presentations, global financial conditions will ease, restore fund flows to Indian markets, and allow for some more injection of ‘animal spirits’ locally. Indeed, the enhanced focus on government as facilitator rather than spender of last resort was clear to us in the budget and seems exactly the right thing to do.

Bond Market Specific Factors

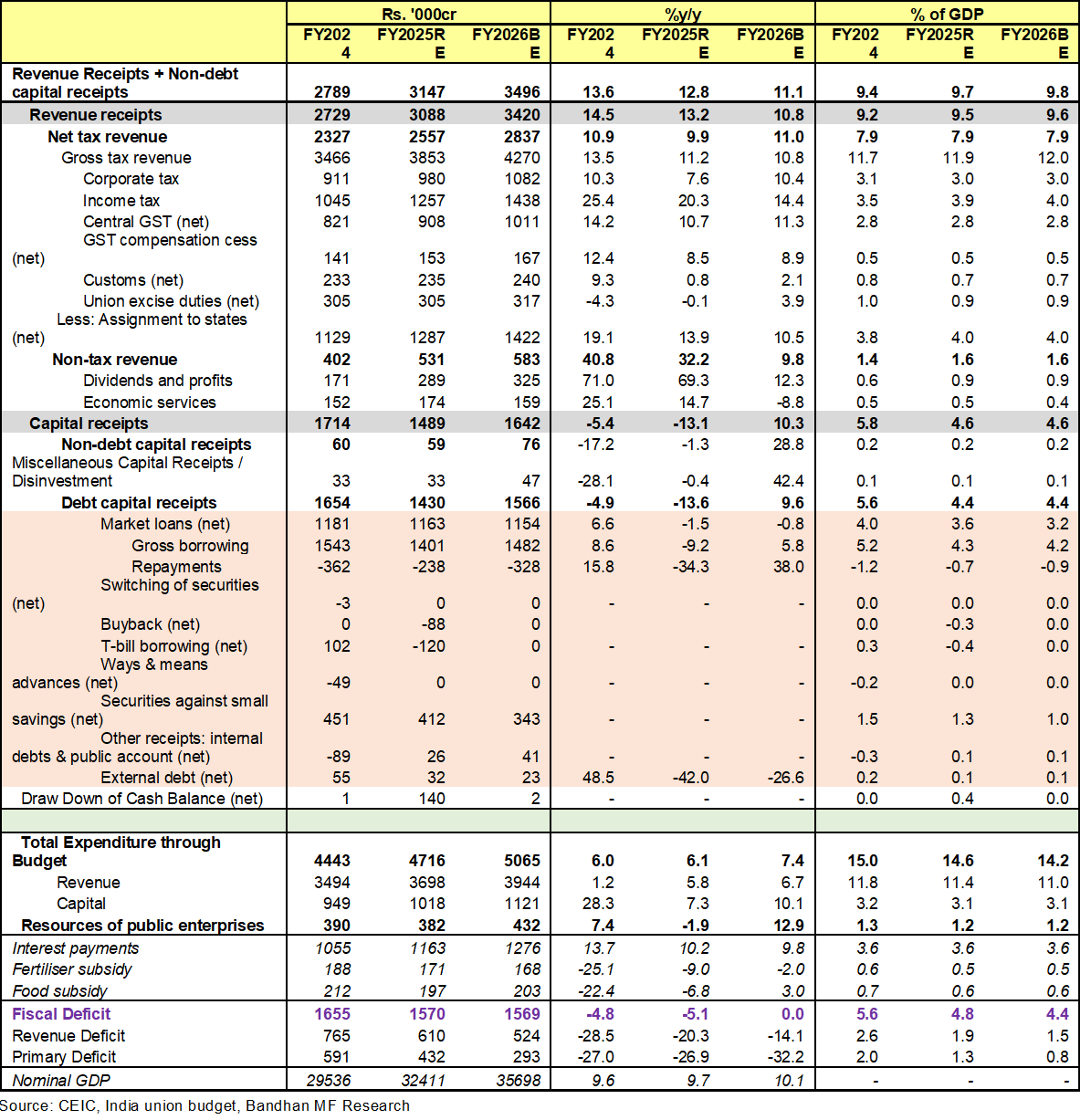

From a more macro assessment, we now turn to the micros of the budget more of immediate interest to the bond market. The budget numbers are summarised below:

Market will like the deficit number and medium term investors will appreciate the debt / GDP framework. From a very short term consideration, however, the borrowing number is approximately INR 50,000 – 75,000 crores higher than what most in the market would have hoped for. That said, RBI has already purchased INR 50,000 crores plus of bonds under OMO with another INR 40,000 crores to go of announced OMOs. Also, while cumulative term plus permanent liquidity infusion steps thus far announced and/ or implemented since January amount to approximately INR 2 lakh crores, more is needed in our view especially if a rate cut is around the corner and the central bank would then want to ensure transmission via keeping liquidity adequately surplus. Thus, and absent adverse global developments, local bond gyrations should remain contained with the medium term bullish view very much intact post the budget. A final point: the gross number for bond switches is pegged at INR 2,50,000 crores. This is quite large and is needed in view of substantial maturities lined up over the next few years that need smoothening. However, a substantial portion of this may entail direct switches with RBI and to that extent will not constitute duration supply to the market. Source: RBI and Bandhan internal research (1st Feb 2025)

Disclaimer:

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

The Disclosures of opinions/in house views/strategy incorporated herein is provided solely to enhance the transparency about the investment strategy / theme of the Scheme and should not be treated as endorsement of the views / opinions or as an investment advice. This document should not be construed as a research report or a recommendation to buy or sell any security. This document has been prepared on the basis of information, which is already available in publicly accessible media or developed through analysis of Bandhan Mutual Fund (formerly known as IDFC Mutual Fund). The information/ views / opinions provided is for informative purpose only and may have ceased to be current by the time it may reach the recipient, which should be taken into account before interpreting this document. The recipient should note and understand that the information provided above may not contain all the material aspects relevant for making an investment decision and the security, if any, may or may not continue to form part of the scheme’s portfolio in future. Investors are advised to consult their own investment advisor before making any investment decision in light of their risk appetite, investment goals and horizon. The decision of the Investment Manager may not always be profitable; as such decisions are based on the prevailing market conditions and the understanding of the Investment Manager. Actual market movements may vary from the anticipated trends. This information is subject to change without any prior notice. The Company reserves the right to make modifications and alterations to this statement/document as may be required from time to time. Neither Bandhan Mutual Fund (formerly known as IDFC Mutual Fund)/ Bandhan Mutual Fund Trustee Limited (formerly IDFC AMC Trustee Company Limited) / Bandhan AMC Limited (formerly IDFC Asset Management Company Limited), its Directors or representatives shall be liable for any damages whether direct or indirect, incidental, punitive special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information. Past performance may or may not be sustained in future.